Analysts say the high demand for digital currencies like Bitcoin makes it near inevitable that Australian authorities will be forced to regulate the industry. What is Bitcoin? A digital cryptocurrency It operates on a decentralised peer-to-peer network, with no central authority or government backing They can be bought with fiat currencies like Australian dollars from online exchanges or created through mining

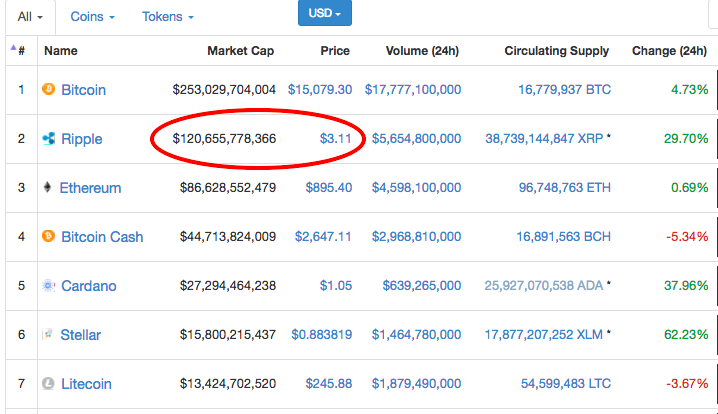

Unlike the coins in your wallet, crypto-currencies only exist online. There are now thousands of different currencies but Bitcoin remains the best-known. Like all currencies, its market value is determined by how much investors are willing to buy and sell for.

Until now, it’s been relatively easy to purchase crypto coins online, using Australian dollars and an online broker — which operates much like a traditional share trading platform.

But over the past few weeks, many Australian cryptocurrency brokers have halted deposits of Australian dollars.

The brokers, including traders such as CoinSpot, are blaming Australian banks for being “unwilling to work” with the digital currency industry.

As investors continue flocking to cryptocurrencies such as Bitcoin and Etherium, questions are being raised about the industry’s ability to operate in a “self-regulated” environment.

The recent surge in popularity of Bitcoin, especially, has seen scores of online brokerages emerge, and many have struggled to keep up with demand.

CoinSpot, one of the country’s most popular digital currency trading outlets, suspended Australian deposits in December.

CoinSpot claimed Australian banks had been “unwilling to work” with the cryptocurrency industry.

The company said this lack of cooperation from the banks was leading to “frequent account closures” and “strict limits” on accounts while they remained operational.

The ‘murky’ world of cryptocurrencies

So why have Australian banks been hesitant to get involved in the cryptocurrency trade?

University of Technology Sydney senior finance lecturer Adrian Lee says it is due to a lack of regulation.

“There’s this murky issue of you buying something that doesn’t have any regulatory backing, and can be transferred off to do something else,” Dr Lee told ABC NewsRadio.

Blockchain Australia Association president Adam Poulton says it is understandable that banks are nervous.

“The volumes have grown so quickly and the number of people using these services have grown so quickly,” he said.

“It’s raised a lot of red flags with the banks. They’re just seeing hundreds of thousands of dollars per day, and they’re like ‘what’s going on here? It looks like fraudulent activity, so we’ll just suspend things for a little while’.”

Most industry insiders say the banking boycott was expected, and that brokers and bankers are trying to negotiate a path through the cryptocurrency boom.

Mr Poulton says smaller brokers have been overwhelmed by the update in cryptocurrency.

“The big established players are set up really well.

They have lawyers and accountants involved and they’ve done everything properly,” he said.

“But compared to a large financial [company] they are pretty small and have limited resources.” Can’t tell a bitcoin from a blockchain? Read our explainer to see how the cryptocurrency works.

Even though many of these smaller trading houses have halted trading in cryptocurrencies, they continue to accept new client registrations — and deposits, in some cases.

Analysts say the high demand for the digital money means it is near inevitable that Australian authorities will be forced to regulate the industry.

In fact, many Australian crypto traders are already trying to operate within a ‘self-regulatory framework’, in part so they can prepare themselves for when the government does legislate.

Dr Lee says over-regulation or the closure of crypto exchanges could stifle the industry and drive it underground, leaving ‘mum and dad’ investors exposed.

But he maintains any regulatory framework must be stringent enough to protect consumers against blind investment and speculative bubbles.

“It’s pretty touchy. You do want to support [the industry] but at the same time it is a big risk for people trading it. They should know that,” he said.

.